We spoke to Craig Solomon, CEO of Square Mile Capital, about how the outbreak of COVID-19 has created challenges and opportunities within the private real estate debt market, and what’s next for the industry

We spoke to Craig Solomon, CEO of Square Mile Capital, about how the outbreak of COVID-19 has created challenges and opportunities within the private real estate debt market, and what’s next for the industry

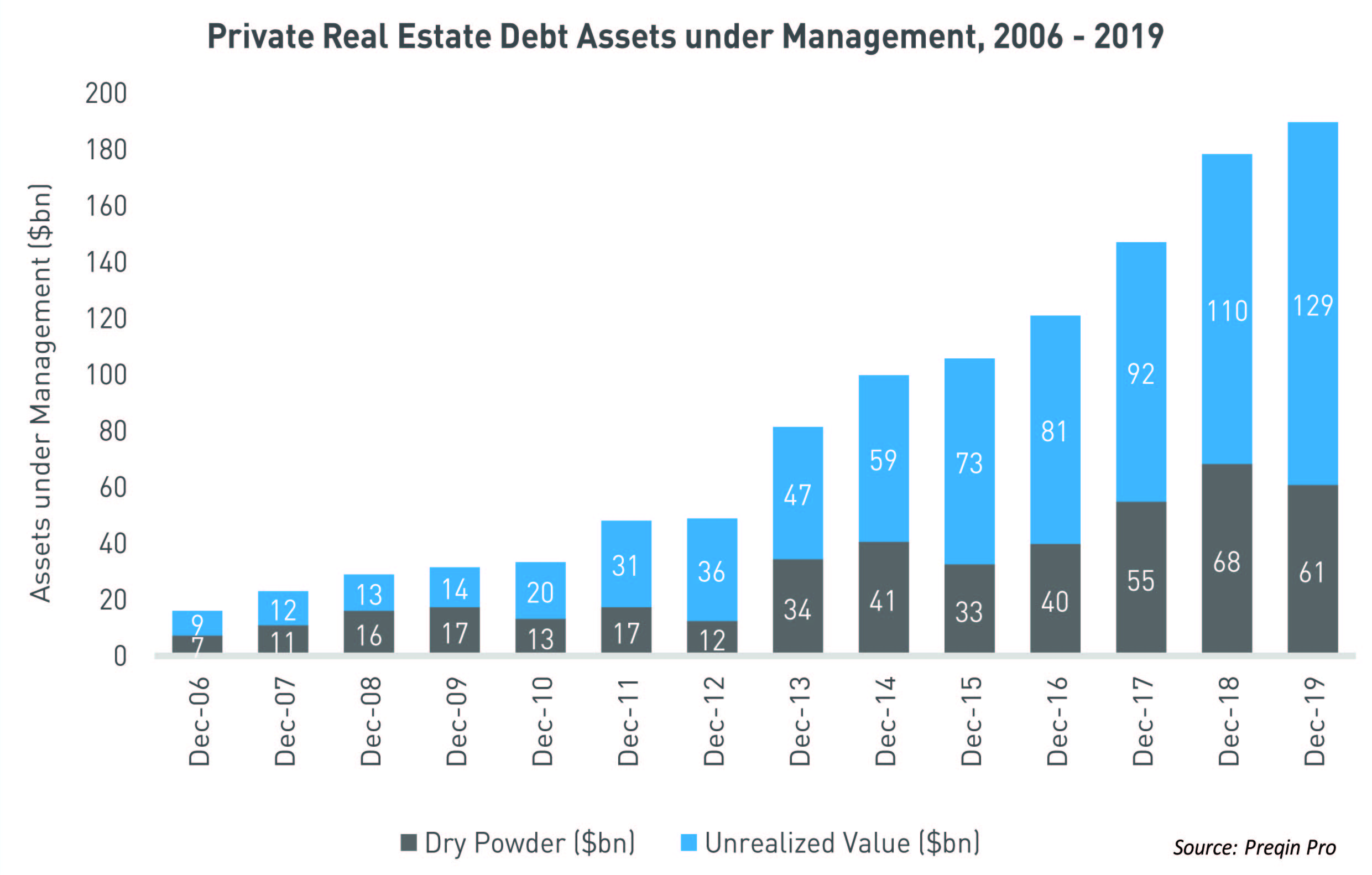

Private lending has been one of the standout growth stories in private real estate over the past decade. Over 1,000 institutions currently allocate to private real estate debt, and as of December 2019, the industry stands at $190bn in aggregate assets under management – doubling in size since 2014. But the sudden onset of the coronavirus pandemic and the ensuing economic slowdown have created the private lending industry’s first significant challenge.

What is your view on the real estate market? What impact has the COVID-19 crisis had?

Prior to the coronavirus pandemic, consensus was that we were late in the cycle. But fundamentals were generally strong, supply and demand were generally in equilibrium, and the real estate industry was benefiting from a historically low interest rate environment as a result of government intervention and little if any inflationary pressures. For any major change in valuations we would have needed some form of catalyst – a so-called black swan.

The outbreak of COVID-19 is that catalyst, and now everything has changed.

The pandemic looks to have brought an end, at least for the time being, to a 10-year run of increasing valuations and activity in the private real estate market. But it is important to note that this is a health crisis, not a financial crisis.

How quickly we return to ‘normal’ and what the ‘new normal’ may look like is yet to be seen.

What are the challenges in the market for private real estate debt fund managers?

Real estate debt fund managers face at least four specific challenges – each to varying degrees.

First, as a leveraged strategy, debt funds must manage through their own leverage issues. Those that overly relied on the use of mark-to-market recourse borrowing and CLOs face liquidity challenges as their funding sources demand paydowns.

Second, consistent lending requires price discovery – what spreads are necessary to compensate for market risk and where do debt fund managers need to price their debt in order to be competitive? The answers to both require transaction volume which is currently constrained.

Third, prudent lenders must underwrite, among other things, market rents and leasing velocity, static vacancy and capitalization rates in order to assess value. In the midst of the pandemic underwriting value is almost guesswork with leasing ground to a near halt and pre-COVID-19 ‘comparables’ of little use going forward.

Finally, debt managers are for the first time dealing with the asset management challenges of loan defaults, the need for loan modifications, and the exercise of remedies.

Where are you seeing opportunities in the private real estate debt industry?

Broadly speaking, as the post-COVID-19 market unfolds and valuations stabilize, those lenders who prudently managed their own leverage and are not faced with their own liquidity challenges are well poised to gain market share as the real estate markets settle into a new normal and transaction volume picks up.

I suspect that the opportunity will be less about wider yields and more about the ability to make loans at more conservative LTVs, with better structure and for higher-quality projects and sponsors. With credit tightening, I see significant opportunity to fill an inevitable void in construction lending as well as in specialty asset classes – notably senior and student housing.

Will the pandemic stunt the growth of the private real estate debt market?

An important aspect of the private lending market is that the private lending universe occupies a very small percentage of the overall real estate debt market.

You have bank lending, insurance company lending, commercial mortgage-backed securities, and then private lending. So the private market still takes a very small slice of the pie, and the opportunity remains broad. Even in a post-COVID-19 world, the question is less about competition and more about who is going to successfully navigate the challenges in their existing loan portfolios as borrower defaults inevitably increase, and how private lenders are themselves financed under current conditions.

Who will be the winners in private debt?

Coming out of the crisis, the private lenders best positioned to gain market share will be the ones that can maintain the best ‘cost of funds’ and simultaneously manage through portfolio stress. Debt fund managers with demonstrable experience in workouts, restructurings, the enforcement of remedies, and the creation of value will outperform.

Another consideration with regard to growth is that it can depend on the specific manager. Not all fund managers are equal. A lot depends on whether the marketplace views the lender as reliable: if a fund manager quotes terms on a loan, they must be able to deliver. Reliability is paramount given that a shake-up among debt fund managers is inevitable.

The managers with the best infrastructure, a stable balance sheet, and a strong brand reputation are positioned for success and to compete for what may be a smaller pool of institutional capital allocating to loan origination strategies, as lending strategy returns are weighed against returns available in distressed equity and other commercial real estate investment strategies.

What’s next for private real estate debt?

For many, a period of growing loan defaults as the economy continues to worsen will require managers to firm up their own balance sheets in the face of margin calls and rebalancing arrangements. For those that successfully maneuver through this crisis, the opportunities will be significant.

In short, the private real estate debt market is here to stay. It will occupy a meaningful – and probably growing – percentage of the overall commercial real estate debt market. The considerations become whether the returns will remain satisfactory over time relative to the risk, and which of the private lenders will survive the crisis.

If the profits that are available to a lender decline, then it will be a matter of whether or not the institutional capital worldwide finds those spreads satisfactory in comparison with other opportunities. Investors active in private real estate debt are focused on the current return of their investment, rather than having a view on long-term equity appreciation. As such, treasury bonds and government yields are typically used as the benchmark for returns. And with government bonds showing low yields in the US, and even negative yields in some cases in Europe, the ability to produce high single-digit returns should remain attractive.

About Square Mile Capital Management LLC

Square Mile Capital is an integrated institutional real estate and investment management firm based in New York. The firm has an established history of successful investing in commercial real estate at all points in the market cycle. Square Mile Capital's experience supplying flexible equity and debt capital solutions in diverse property sectors and across the risk spectrum, combined with its national investment platform, facilitates the creation of value for our investors, partners, borrowers, and counterparties.

This article is the third in a series analyzing the impact of COVID-19 on the private real estate market, produced in collaboration with our partner EisnerAmper. We discuss deals, fundraising, and other key trends in the industry.

To ensure you don’t miss the next installment in this series, sign up for Preqin’s weekly newsletter.

For more insights and analysis on the impact of the pandemic on alternative assets, take a look at our COVID-19 Knowledge Hub.