Follow DoorDash and its investors from private funding to IPO

Follow DoorDash and its investors from private funding to IPO

DoorDash

San Francisco-based DoorDash launched in 2013 as an online service delivering food to customers from local restaurants. The company’s business model paired the on-demand goods delivery concept pioneered by Amazon with the on-demand service concept made popular by ride-share provider Uber, which itself soon started competing via Uber Eats in August of 2014.

DoorDash’s nine-year history shows the company moving from tech start-up to a $10bn valuation at the last venture round and an eventual IPO, when the valuation was over $30bn. Preqin’s Company Intelligence charts that journey.

An appetite for growth

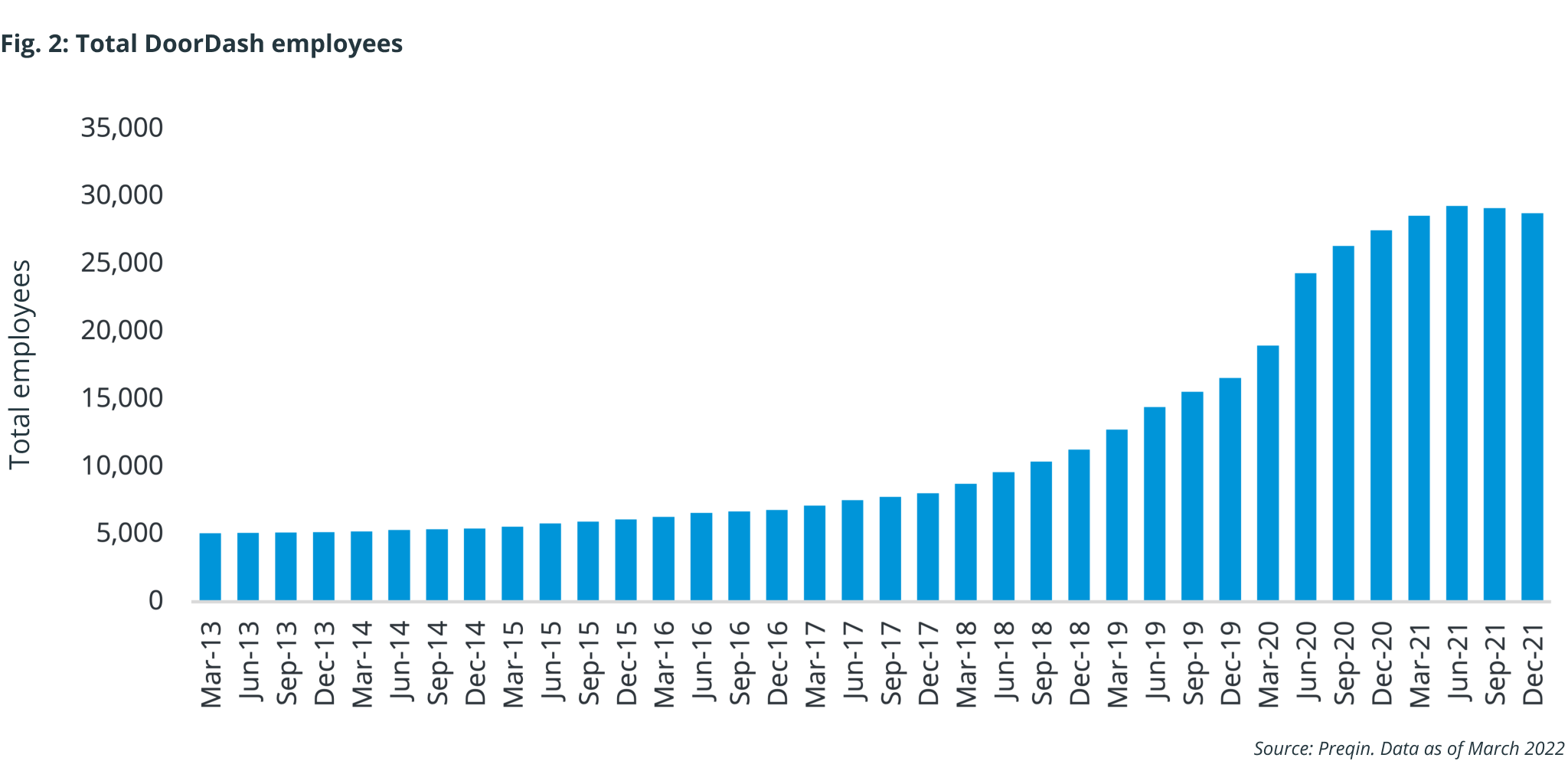

The model, simple as it was, worked. The company’s mobile app aggregates local menus for prospective diners, lets them order and pay, then delivers their meal to their door. The app’s success drove positive revenue growth which needed to be satiated by an ever-growing number of drivers – Dashers in company parlance. The company grew from 5,000 employees in 2013 to 8,000 by the end of 2017 (Fig. 2), before a rapid escalation to near 30,000 in 2020, after it secured substantial funding in 2018. The company’s delivery drivers are independent contractors, with six million dashers completing at least one delivery in 2021. DoorDash says the arrangement offers flexible and attractive opportunities that enable people to meet their goals.

Like many start-ups, DoorDash initially operated on low margins, and frequently negative net earnings. Revenue was driven by commissions on customer orders, typically 3% to 5%, which would in turn be used to pay drivers and fund operations. However, the early revenue growth was hardly enough to keep up with DoorDash’s aspirations.

From seed deal to IPO

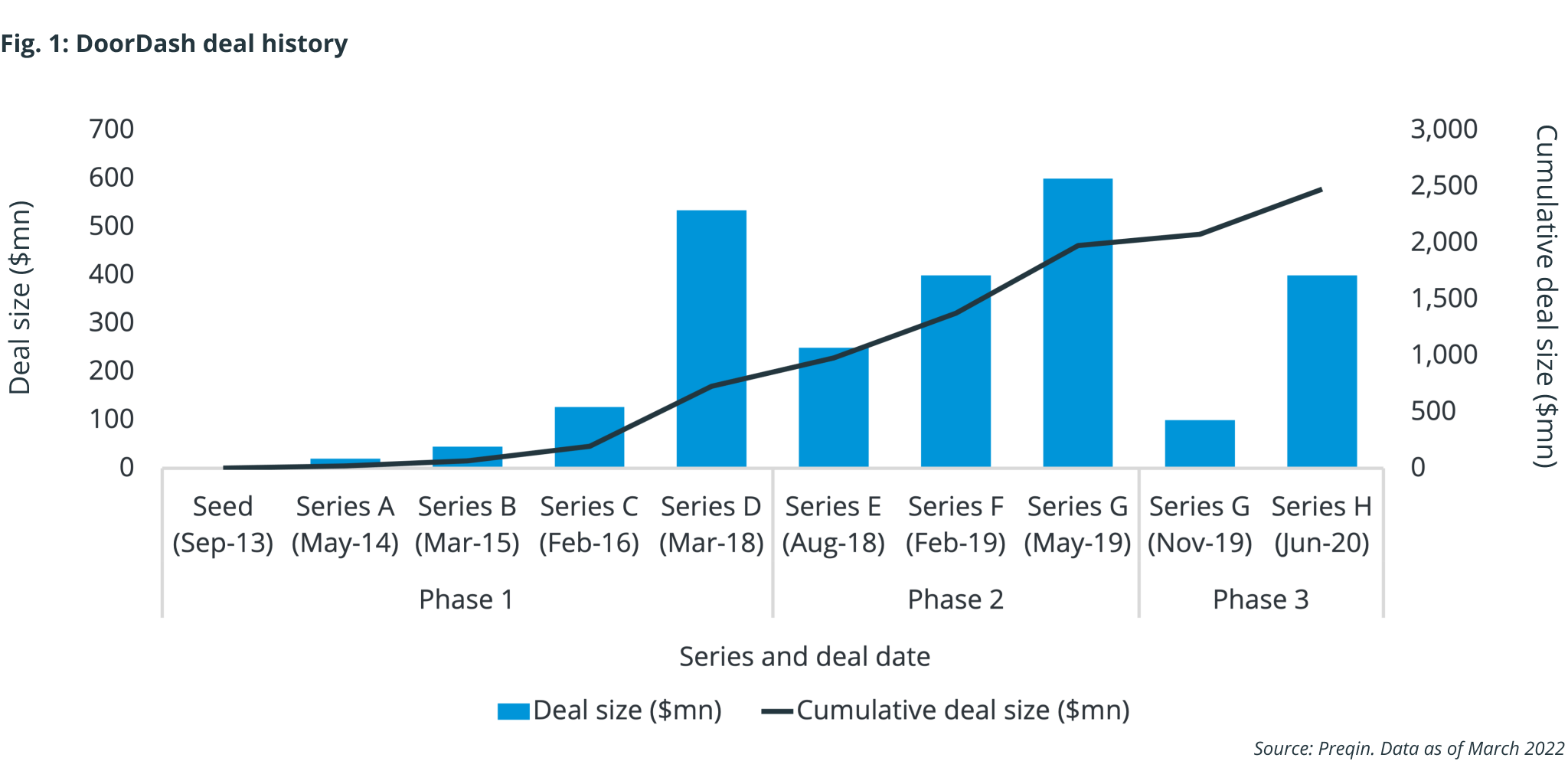

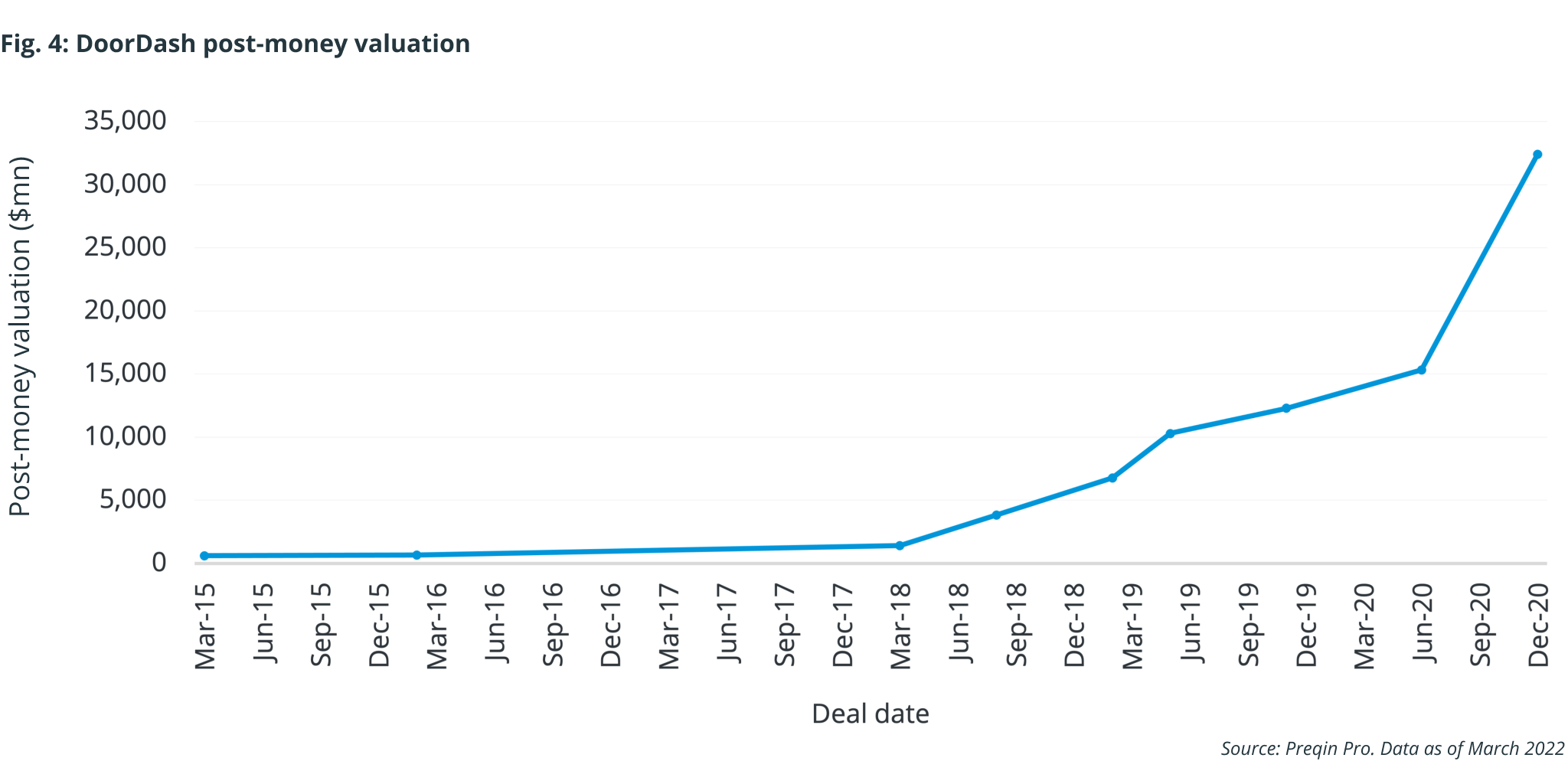

To meet these objectives, DoorDash raised a steady flow of capital between its 2013 founding and its December 2020 IPO across three phases (Fig. 1). Between September 2013 and March 2018, the founders raised $729mn across five transactions and 23 investors. This led to a $1.4bn post-money valuation (Fig. 4), following $535mn in series D funding in the first quarter of 2018. It was what’s commonly known as a unicorn.

Among the investors was Khosla Ventures, who took part in the $2.4mn seed deal and across the next three rounds, culminating in the $127mn series C round. Also providing capital was early-stage venture capital specialist Sequoia Capital, participating in four of DoorDash’s first five rounds between series A and series D funding.

It was in this first phase that DoorDash made its first acquisition, buying delivery and logistics tech company Rickshaw in September 2017. The acquisition enabled DoorDash to develop a product which allowed customers to leverage DoorDash’s network for their own delivery purposes. At the time, Tech Crunch noted that the companies were familiar with each other. DoorDash was working on similar same-day delivery technology, which they called Drive. DoorDash CEO Tony Xu referred to the transaction as an “aquihire” in a blog post, pointing to close ties since the companies’ time with incubator Y Combinator. While the deal effectively dissolved Rickshaw’s operations, there were several common investors between the two including Khosla, Sequoia, CRV, and Streamlined Ventures.

Phase two – the main course

The next phase of DoorDash’s journey saw a faster rise in funding and implied company value. Following March 2018’s $535mn series D capital injection, that summer DST Global and Coatue Management put $250mn of series E funding into DoorDash. That year, the earliest available earnings results, saw the company report a revenue of $291mn while also reporting a net loss of $204mn, even as August’s series E funding valued the company at an estimated $3.8bn.

Losses like these are common for venture-backed companies. In 2019, Preqin data shows that DoorDash revenues rose to $885mn, a 204% year-over-year increase, but also a $616mn operating loss. In the public markets performance like this would deter significant investment, but this logic doesn’t always apply in private markets. Or in consumer tech, where customer growth can take precedence over profits. Indeed, according to DoorDash’s 2020 annual report, total orders jumped to 263 million in 2019 from 83 million the year before. The gross order value, a metric the company uses to gauge how much its customers are ordering, rose to more than $8bn in 2019, from $2.8bn in 2018. Buried in that growth, however, were hints of a shift in the market affecting pricing power. Even as the volume of orders rose 216%, the value of those orders lagged, relatively, at 185% growth.

That year the company raised another $1.1bn in capital including $1bn across two deals in the first half of 2019, driving DoorDash’s post-money valuation to an estimated $12bn.

Phase three – the icing on the cake

The 15 months that followed comprised the final phase of DoorDash’s seed-to-IPO journey. T. Rowe Price, a manager typically associated with public-market investments, but with a strong record in growth-oriented assets, ended 2019 with a single $100mn series-H investment. However, the onset of COVID-19-induced lockdowns drove the company’s financials to new levels. Revenues jumped to $2.9bn in 2020 from $885mn in 2019, as quarantining users ordered a collective $25bn in deliveries. For perspective, that is more than the 2021 national gross domestic product of Iceland.

DoorDash achieved its first ever quarterly net profit in the second quarter of 2020, when company financials reported $23mn in net income (unaudited) on $675mn in revenue. While the following quarters saw net income figures dip below zero again, EBITDA remained positive.

The company’s estimated value would rise to $15.3bn after a final $400mn, series H round involving T. Rowe Price, Fidelity, and Durable Capital Partners in June 2020. That year, during which the COVID-19 pandemic touched every aspect of global life, was particularly strong for DoorDash. The company’s model was tailor-made for the conditions created by stay-at-home orders and lockdowns. Customers still had access to local restaurants and grocery, while partner businesses were given a lifeline as eat-in dining business evaporated.

Food for thought

That year ended with a 33 million share IPO that raised an estimated $3.4bn for the company, or 10% of the company’s $32bn equity value at the time. The period that followed saw two more acquisitions but muted public equity performance.

The first of these acquisitions was the February 2021 acquisition of Chowbotics, maker of Sally the robot salad chef. Terms of the deal were not reported, but CI shows that partners included T. Rowe Price, Fidelity, and Durable Capital Partners. The other was a deal for Finnish delivery-app peer Wolt Enterprises Oy in November 2021. This acquisition, which renamed Wolt to DoorDash International, gave DoorDash a foothold in Europe, expanding its reach beyond North America, Australia, and Japan.

Will the efforts of DoorDash’s founders and its private capital partners pay off? The results are yet to be seen. Since its IPO, DoorDash’s public equity has traded as much as 42%¹ lower and 41% higher than its $182 per-share NYSE debut, though a 57% fall over the three months to March 2022 is considerably sharper than the 16% experienced by Nasdaq Composite. During that time margins have struggled to improve because of intense competition, despite the company’s 58% market share in January 2022, well ahead of rivals Uber Eats (24%) and Grubhub (15%), according to analysis by Bloomberg Second Measure.

The company’s most recently announced year-end 2021 earnings show key metrics like revenue, order volume, and gross order value all at new highs, although year-over-year growth looks to be slowing. Gross order value was high at $11bn in the fourth quarter, but the 36% year-over-year percent change fell from Q3 (44%) and also from Q4 2020 (227%). Revenue growth experienced similar effects while profit margin growth has struggled to improve.

The story of DoorDash is one of many that Preqin’s Company Intelligence can tell. Looking into who is investing in a company, how much they are committing, and where else they, or their peers, have similar bets, can offer insight into a manager's portfolio. When aggregated, the user can see networks form, linking portfolio companies across investors and identifying trends across the private capital industry.

What is Company Intelligence?

In 2021 Preqin launched Company Intelligence (CI) to improve the transparency of portfolio companies, their private capital partners, and investors. Our data profiles companies, enabling comprehensive due diligence and deal sourcing as well as insights on how, when, and why managers deploy capital and exit investments.

Power your deal-making with accurate and comprehensive private market data and intelligence on investor-backed companies. Get a complete view of the private capital lifecycle with interconnected company, fund and performance data. Find out more about Company Intelligence today.

¹DoorDash (DASH) equity return since IPO as of 3 March 2022.