As APAC’s private debt industry reaches an inflection point amid rising rates and falling equity valuations, managers are optimistic about the expansion of the asset class

As APAC’s private debt industry reaches an inflection point amid rising rates and falling equity valuations, managers are optimistic about the expansion of the asset class

Private debt can offer investors portfolio diversification and higher yields in today’s inflationary environment. With equity valuations falling, private debt offers global investors an alternative, on the back of existing strong growth. In Japan, South Korea, and Australia, private debt has grown alongside stronger M&A and private equity-backed buyout deal activity.

Demand for financing has increased in these markets. However, private debt funds have made substantial inroads into what was once a bank-dominated market. Private equity sponsors value the flexibility of private debt and the alignment they have with lenders in these transactions. In APAC, however, there is still some way to go to increase penetration into the wider corporate market, where the higher cost compared with bank debt tends to deter companies.

Private debt in APAC nonetheless benefits from the global trend of tighter bank lending conditions, which have increased demand for private debt from mid-market corporates. SMEs account for an average 96% of all enterprises and 62% of national labor forces, and they are in urgent need of working capital. The lack of access to finance is one of the major barriers to recovery cited by SMEs, according to a 2021 survey by Asia Development Bank.

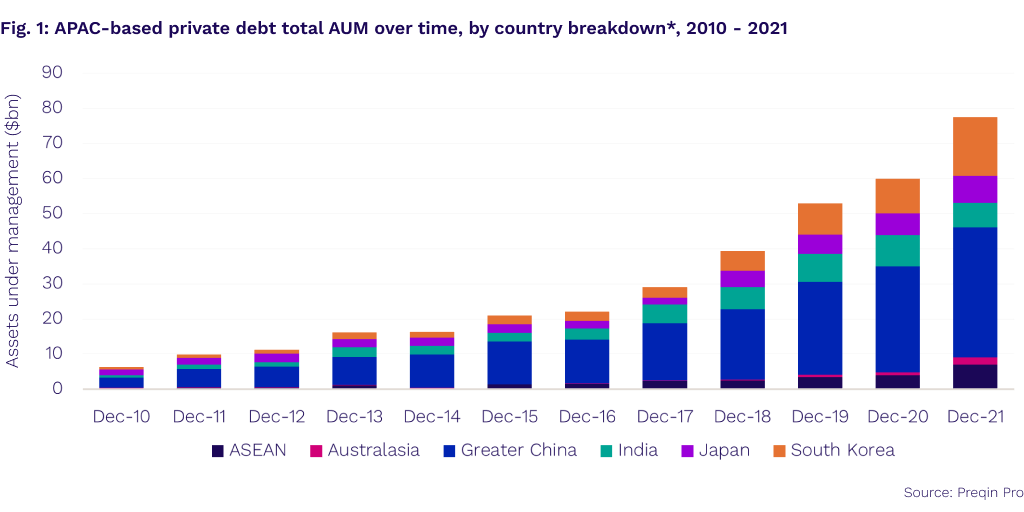

APAC-based private debt AUM stands at $78bn as of December 2021 and has grown at an average rate of 29% over the past five years, faster than the global average of 17% over the same period (Fig. 1). With APAC-based AUM constituting just 6% of the global total, there is plenty of room for growth. Discover more data and insights on private debt in APAC through our latest report Preqin Territory Guide: Private Debt in APAC 2022.

We asked three private debt players for their views on the current market conditions, the upcoming deal pipeline, and how they think PD managers can position themselves to appeal to LPs.

_______________________________________________________________________________________________

Andrew Lockhart, Managing Partner at Metrics Credit Partners, an Australia-based private credit firm

With the current rates of inflation in the global market, there will be a slowdown in economic activity due to inflation curbing demand. The Reserve Bank of Australia is trying to reduce demand and slow economic activity with the increase of interest rates. But the rising rates benefit private debt because investors can make use of floating-rate facilities.

For us, the extent of the opportunity is large given the current regulatory environment, cost of capital, and the difficulty of borrowing from banks in Australia. Despite the recent growing attention, this trend has been happening since the 2007 to 2008 Global Financial Crisis.

There has been a lot of interest from Australia’s domestic LPs, including insurance providers. However, we see more interest among offshore LPs, including Japan- and New Zealand-based investors. We present an attractive option to them. In the next 12 months, Metrics looks to raise capital in other offshore markets.

To attract investors, we need to demonstrate that we have a strong record of delivery. Investors in more traditional asset classes, such as bonds, hybrids, or public market securities, are now looking for private-market investment options. In addition, they are seeking a large scalable team that has a demonstrable track record. I believe there are benefits of size and scale that deliver diversification, better risk management, and direct origination. These drive return outcomes for our investors that are likely to continue. In the last 12 months, we have completed AUD $6.5bn of transactions across more than 200 individual loans as a business. What’s more, our current pipeline exceeds AUD $9bn.

We have invested substantially in direct origination to find suitable opportunities and are focused on preserving investor capital and providing funding to businesses. Our funds have comfortably exceeded their returns, but the key remains in identifying direct origination opportunities and managing risk.

_______________________________________________________________________________________________

Younghwan Han, Head of VIG Alternative Credit, a South Korea-based private debt firm

We are passing through an inflection point in terms of the economic environment. The past era began with the Global Financial Crisis (GFC) and climaxed with COVID-19, where we had a nearly zero-base rate, tight credit spread, and abundant liquidity. The new era is starting with inflation, meaning a sharp increase in the base rate, daily widening of the credit spread, and liquidity drying up everywhere. While the recent past was a golden age for equity investors; we believe the new era will be the one for credit investors.

Market uncertainty is peaking, and this is creating opportunities for special situations and other opportunistic credit investments with a full distressed cycle coming closer. The key is to select the right target, such as where we see a sound underlying business/asset that’s mispriced due to the market situation. In that situation, the deal pipeline looks sufficiently healthy, if not overwhelming, over the next six months to capture this market dislocation.

Obviously, the market will stabilize at some point and market dislocations will become rarer. However, we believe the new era will not repeat past base rates, credit spreads, and liquidity. Hence, private debt will generally become a more attractive asset class to LPs and the key would be selecting the right GP in each market with tangible value-adding capacity. This will provide the best opportunity of outperforming the market.

_______________________________________________________________________________________________

Insun Mo, Manager at Korean PE firm IMM Investment, ACM Division

Following the revisions to the Financial Investment Services and Capital Markets Act last year, private equity fund managers are now able to deal with both private credit fund and private debt funds. Such financing was previously provided mostly by banks, but now VC and PE funds, as well as large corporations with new business opportunities, can provide finance via private debt issuance. This means that private debt and project financing, which have been active mainly in the real estate market in Korea so far, are expanding to M&A financing and the direct lending market.

Since late 2021, PEVC firms have been setting up new subsidiaries or responsible groups for private credit investments and starting to invest private credit products. These include IMM Credit Solution by IMM PE, the Alternative Capital Market division by IMM Investment, VIG Alternative Credit by VIG Partners, Glenwood Credit by Glenwood PE, and STIC Investment, among others. In addition to local houses, global PE firms are entering Korea, such as Affirma Capital, Stifel Financial (with Korea Investment & Securities), and Apollo Global Management. However, there may still be a long way to go to grow the support business at investment banks, securities firms, and trust and fund services, as well as the capacity to value and source deals to develop the private debt market.

Nevertheless, we are expecting the private debt market in Korea to grow gradually in the next few years for the following reasons:

Lastly, PD allows institutional investors to benefit from new investment opportunities at higher returns with collateral, or some safety measures.

_______________________________________________________________________________________________

Eddie Ong, Deputy CIO and Managing Director, Private Investments at SeaTown Holdings International

Traditionally, private investments in the APAC market are dominated by private equity strategies. Most capital gravitates toward higher return products above 20% IRR or more than 2x MOIC when allocating to illiquid strategies. Therefore, historically, non-distressed private debt pales in return. The last two decades of a low-rate environment have underpinned continued earnings growth and multiples expansion. It’s only until now that global financial markets have taken on a decisive turn for the worse, with inflation and interest rates on a sustained uptrend.

LPs are now waking up to the reality of:

Asia’s private debt markets are more heterogeneous when it comes to legal/enforcement and the characteristics of capital markets compared with the developed markets of the US and Europe. Global LPs now deem savvy private debt structurers to be able to offer attractive risk-adjusted returns, with access to collaterals, covenants, and monitoring systems.

Private debt volume tailwind has continued to pick up post-GFC where the increased capital charge on banks and regulated financial institutions have limited their deployment. The weakened state of global equity markets has pushed many Asia-based mid-market public and private companies to look for private debt as a financing solution, accelerating asset class growth.